Summary: Liability-Only Car Insurance Ratings

Who Has the Cheapest Liability-Only Car Insurance?

USAA, Erie and Auto-Owners are the cheapest companies for liability car insurance among the insurers we analyzed. The following insurers have annual rates less than the national average of $638 per year.

| Company | Average annual cost of liability-only car insurance |

|---|---|

| USAA* | $373 |

| $437 | |

| $445 | |

| $481 | |

| $481 | |

| $617 |

Cheap Liability Car Insurance Companies

See our picks for top-rated liability-only car insurance companies.

What Does Liability-Only Car Insurance Cost?

The average national rate for liability-only car insurance is $638 a year, based on our research. That’s 69% lower than $2,026 a year for full coverage car insurance, on average.

Exact costs vary based on factors that can include:

- The car insurance company.

- Your age and gender.

- Your credit, in states that allow credit to be considered.

- Your driving record.

- Your location.

Liability-Only Car Insurance Costs By State

The cost of liability-only car insurance varies by state. One reason why is that states require different levels of liability coverage to drive legally. Vermont is the state with the lowest rate for liability insurance, $313 per year on average or $26 a month, based on our analysis. Vermont is followed by Iowa, Wyoming, South Dakota and Ohio.

Florida, New Jersey, Michigan, New York and Delaware are the states with highest average rates for liability-only auto insurance, according to our analysis. Florida’s average minimum car insurance cost is $1,529 per year, 388% more than Vermont’s annual cost.

Costs by State for Liability-Only Car Insurance

| State | Average annual minimum car insurance costs | Average monthly minimum car insurance costs |

|---|---|---|

| $578 | $48 | |

| $518 | $43 | |

| $708 | $59 | |

| $550 | $46 | |

| $731 | $61 | |

| $594 | $49 | |

| $1,088 | $91 | |

| $1,107 | $92 | |

| $1,529 | $127 | |

| $815 | $68 | |

| $423 | $35 | |

| $400 | $33 | |

| $629 | $52 | |

| $476 | $40 | |

| $318 | $27 | |

| $600 | $50 | |

| $799 | $67 | |

| $1,060 | $88 | |

| $477 | $40 | |

| $1,004 | $84 | |

| $567 | $47 | |

| $1,173 | $98 | |

| $677 | $56 | |

| $537 | $45 | |

| $726 | $61 | |

| $544 | $45 | |

| $412 | $34 | |

| $920 | $77 | |

| $518 | $43 | |

| $1,237 | $103 | |

| $551 | $46 | |

| $1,114 | $93 | |

| $528 | $44 | |

| $626 | $52 | |

| $389 | $32 | |

| $567 | $47 | |

| $824 | $69 | |

| $530 | $44 | |

| $755 | $63 | |

| $776 | $65 | |

| $381 | $32 | |

| $547 | $46 | |

| $796 | $66 | |

| $771 | $64 | |

| $313 | $26 | |

| $621 | $52 | |

| $547 | $46 | |

| $542 | $45 | |

| $424 | $35 | |

| $319 | $27 |

Liability-Only Car Insurance Costs By Gender

In most states, your gender can help determine your rates. Typically, males will see higher rates than females when they are young drivers. When it comes to car insurance for seniors, males typically pay more for their coverage than female drivers. For the in-between years, males may pay on par or even less than females.

A look at the rates for a 40-year-old female and male driver shows that Allstate and State Farm charge male and female drivers the same amount. Most others charge females slightly more at this age.

Costs by Gender for Liability-Only Car Insurance

| Company | Female average annual car insurance cost | Male average annual car insurance cost |

|---|---|---|

| $899 | $871 | |

| $440 | $440 | |

| $437 | $424 | |

| $925 | $817 | |

| $549 | $526 | |

| $694 | $594 | |

| $708 | $680 | |

| $641 | $608 | |

| $817 | $827 | |

| $613 | $613 | |

| $667 | $661 | |

| USAA* | $357 | $350 |

| $481 | $478 |

How To Find the Cheapest Liability-Only Car Insurance

The best way to find the cheapest liability-only car insurance is to shop around and compare car insurance quotes from multiple car insurance companies.

Request quotes for the same level of liability coverage from each insurance company so you can make an apples-to-apples comparison.

Make sure to maximize any discounts offered by the company. Standard car insurance discounts include:

- Buying multiple policies.

- Insuring more than one vehicle.

- Vehicle safety features, such as anti-lock brakes.

- Having certain anti-theft devices.

- Recent history of being a good driver.

- Paying in full for the policy term.

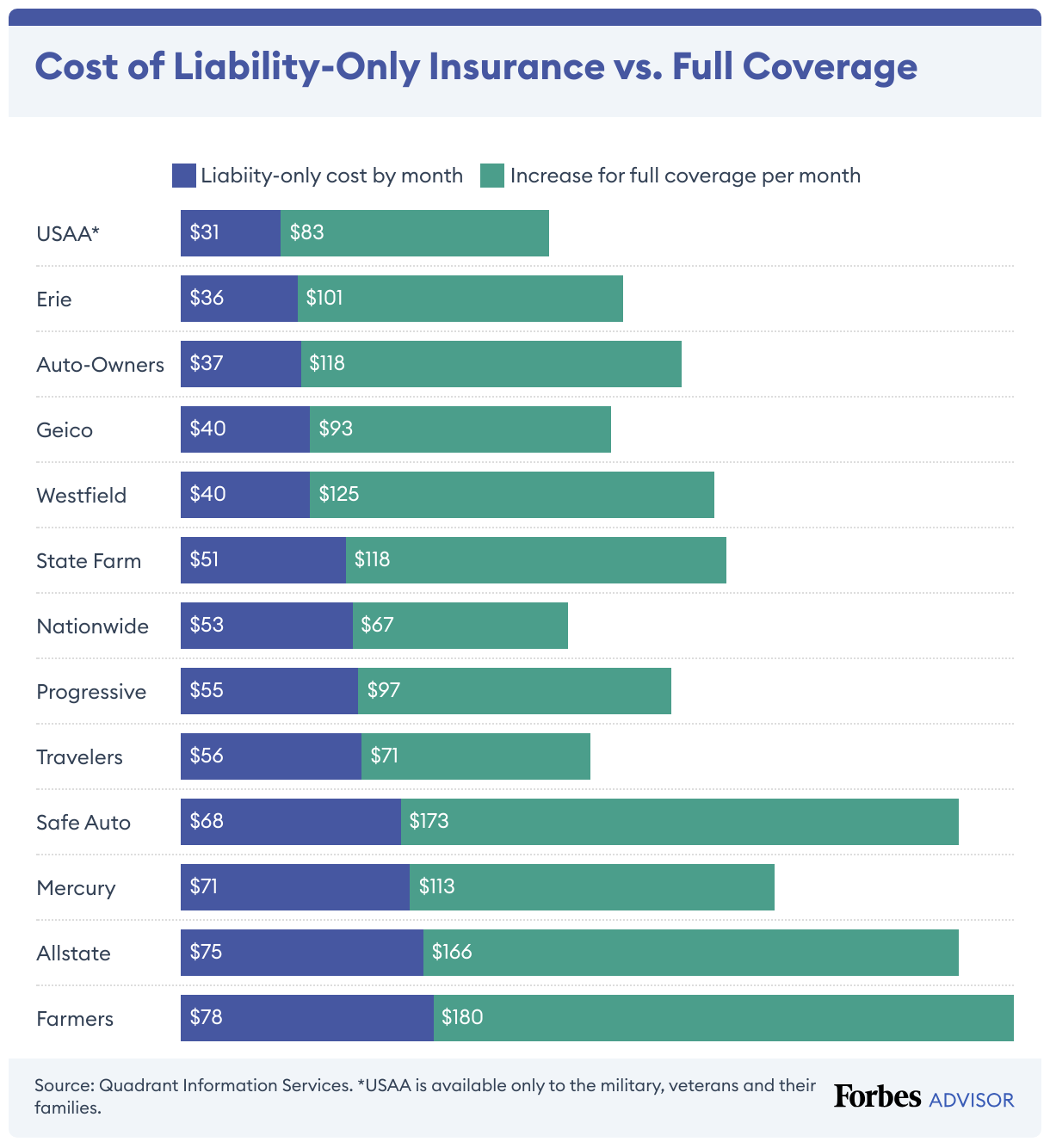

How Much Cheaper Is Liability-Only Coverage?

Liability-only car insurance is substantially cheaper than full coverage: $116 a month cheaper on average, according to our analysis. Liability-only insurance costs an average of $53 a month, while full coverage averages $169 a month.

Full coverage insurance usually has higher liability limits and includes collision and comprehensive insurance. That better coverage comes with higher costs.

Monthly Cost of Liability-Only vs. Full-Coverage Car Insurance

| Company | Average monthly liability-only car insurance cost | Average monthly full coverage car insurance cost |

|---|---|---|

| $75 | $241 | |

| $37 | $155 | |

| $36 | $137 | |

| $78 | $258 | |

| $40 | $133 | |

| $71 | $184 | |

| $53 | $120 | |

| $55 | $152 | |

| $68 | $241 | |

| $51 | $169 | |

| $56 | $127 | |

| USAA* | $31 | $114 |

| $40 | $165 | |

| National Average | $53 | $169 |

*USAA is available only to military members, veterans and their families.

What Does Liability-Only Car Insurance Cover?

Liability-only car insurance covers the damage and injuries you cause others when you’re at fault for an auto accident. There are two different varieties of liability car insurance: bodily injury liability coverage and property damage liability coverage.

How To Read Liability Car Insurance Limits

Car insurance companies package together bodily injury and property damage liability limits using a format like this: 25/50/10. It’s easy to understand once you know what each number signifies.

Liability-only car insurance with 25/50/10 limits means the policy has:

- $25,000 in bodily injury liability coverage per person.

- $50,000 in bodily injury liability coverage per accident.

- $10,000 in property damage liability coverage per accident.

What's Not Included With Liability-Only Car Insurance?

Liability-only car insurance does not include the following, but these coverage types may still be required by a lender or your state.

When To Consider Liability-Only Coverage

Liability-only car insurance may make sense if:

- You can only afford bare-bones coverage.

- You can easily afford to repair or replace your car if it’s damaged or stolen.

- You don’t have a car loan or lease (which generally requires collision and comprehensive insurance).

- You drive an older vehicle that isn’t worth much.

- You would not get your car repaired or replaced if it were damaged or stolen because it has low value.

Is Additional Auto Insurance Required?

How much car insurance you need varies by state. In addition to liability insurance you might have to buy:

- Medical payments insurance. Maine and New Hampshire require medical payments coverage as part of your car insurance policy.

- Personal injury protection. PIP insurance is required in 15 states.

- Uninsured motorist insurance. UIM insurance is required in 21 states and Washington, D.C.

Do I Need Liability-Only or Full Coverage Car Insurance?

You will typically need full coverage car insurance if you have a loan or lease your car. Lenders usually require you to have comprehensive and collision coverage in addition to liability insurance.

If you own your car but you don’t have enough savings to pay to repair or replace it, you likely want full coverage car insurance. It can help reduce out-of-pocket costs if your car is damaged, stolen or totaled.

Liability-only car insurance is best suited for those who would not fix or replace their car if it was damaged or totaled, or who drive an older car that isn’t worth much. Weigh the costs vs. the possible maximum benefits when considering liability vs. full coverage car insurance.

Who Should Buy Only the Minimum Liability Insurance?

Drivers who don’t need coverage for their cars and who have little to lose if sued after an accident are good candidates for minimum liability insurance auto policies.

While it may be tempting to buy state minimum auto coverage to save money on premiums, it’s crucial to remember the low limits of these policies can leave you financially vulnerable after a car accident.

For example, if your state’s minimum coverage limits are 25/50/10, this would provide only up to $25,000 for injuries per person to others and only up to $50,000 for injuries per accident. With the high cost of medical care, an accident that results in injuries could surpass these limits. A good rule of thumb is to buy enough liability insurance to cover what could be taken from you in a lawsuit.

Liability-only auto insurance and state minimum coverage may be a good fit for car owners who do not have the budget to buy more insurance than they are legally required to have. Minimal insurance is certainly better than none.

However, almost everyone else would be significantly better off with a more robust auto insurance policy that has higher limits for bodily injury liability coverage and property damage liability coverage, as well as full coverage options like collision and comprehensive coverage.

How to Find the Best Liability-Only Car Insurance

Penny Gusner

Insurance Senior Writer

Amy Danise

Insurance Managing Editor

Les Masterson

Insurance Editor

Michelle Megna

Insurance Lead Editor

Jason Metz

Insurance Lead Editor

Shop Around

Getting multiple car insurance quotes is the best way to find the best price for liability-only or any type of auto policy. Companies calculate rates differently, so I always want to see which insurer offers the lowest cost by getting quotes from at least three companies.

Insurance Senior Writer

Look at Limits

A liability-only policy may be all you can afford right now, but look at the limits and see if you have room to exceed the state minimum. I recommend buying as much liability coverage as your budget permits because having inadequate coverage could be disastrous for your finances if you cause a major accident.

Insurance Managing Editor

Ask About Discounts

A bare-bones auto policy is the cheapest type to buy, but you can see if you can lower your rates even more with discounts. I double-check with my agent to make certain I’m getting all the auto insurance discounts I’m eligible for.

Insurance Editor

Reconsider Coverage if Your Situation Changes

Liability-only insurance gives you the least amount of coverage your state will allow. If something changes—say you buy a newer car—I suggest you consider adding comprehensive and collision insurance. These coverage types help pay for repairs if your car is damaged in an accident you cause or by non-crash events, like flooding or hail.

Insurance Lead Editor

Talk to an Agent

You can compare quotes online to see what company offers the best prices for liability-only insurance, but you can also talk to an independent agent. They work with multiple companies and can help you find the best deal by providing quotes from many companies. They can also match your driver profile to a company that best suits your needs and offer tips to lower car insurance costs.

Insurance Lead Editor

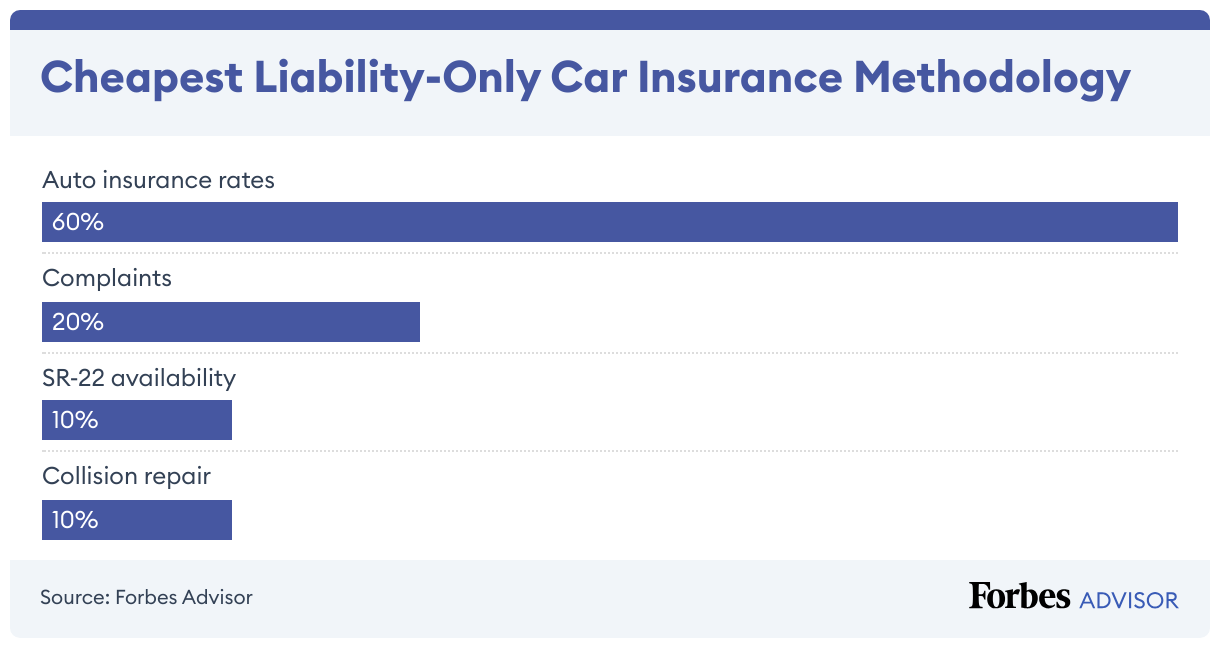

Methodology

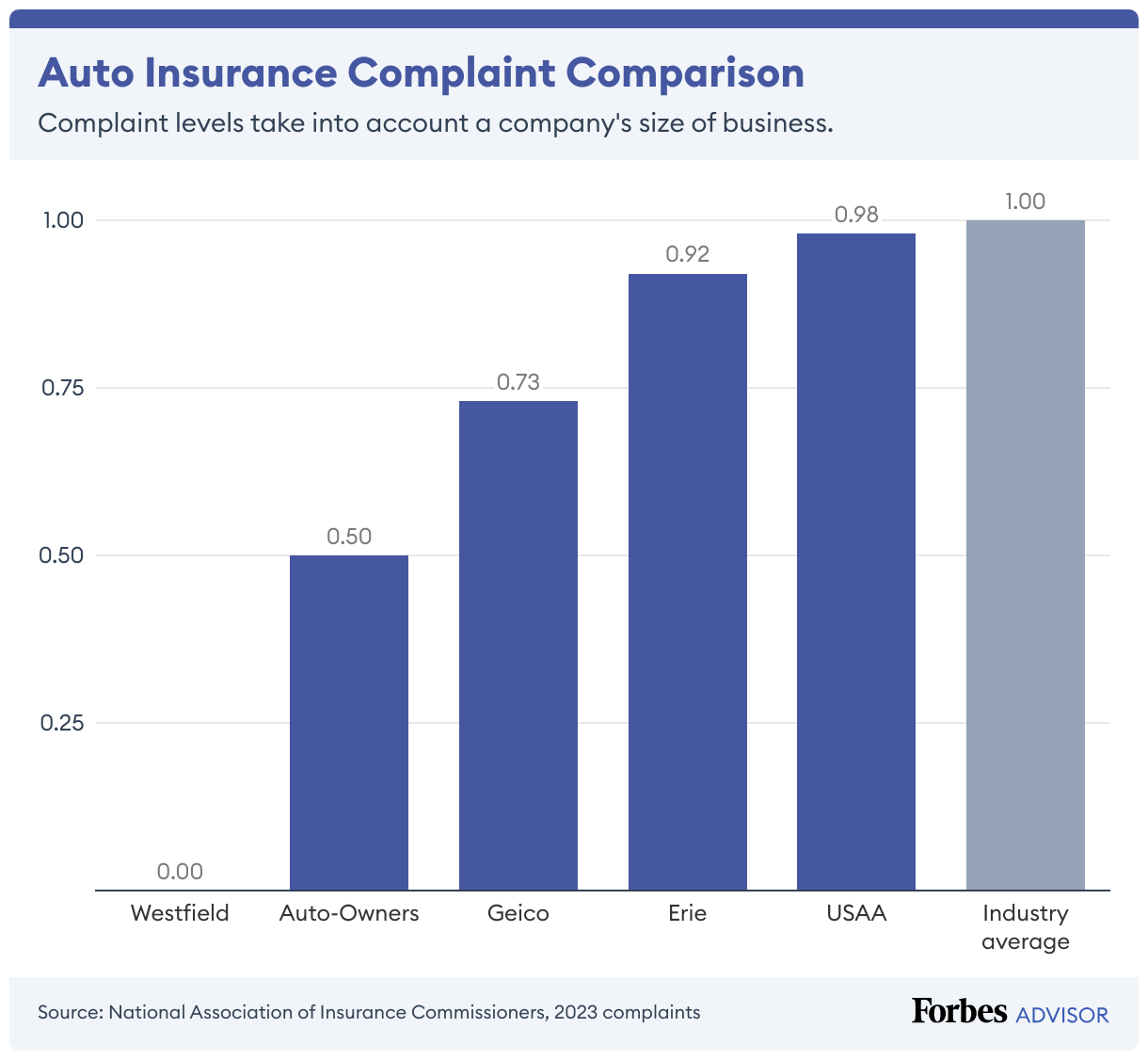

To identify the best liability-only car insurance companies, we evaluated each company based on the average rates for state-minimum car insurance, complaints against the company, SR-22 availability and collision repair grades from auto body professionals.

Car insurance rates (60% of score): We used data from Quadrant Information Services to find average rates from each company for the minimum amount of auto insurance required in each state. Rates are based on a 40-year-old female driver with a Toyota RAV4.

Complaints (20% of score): We used complaint data from the National Association of Insurance Commissioners. Each state’s department of insurance is in charge of logging and monitoring complaints against the companies that operate in their states. Most auto insurance complaints center on claims, including unsatisfactory settlements, delays and denials.

The industry complaint average is 1.00, so companies with a ratio below 1.00 have lower levels of complaints.

SR-22 availability (10% of score): We gave points to insurers that offer SR-22 insurance. An SR-22 is a form that an insurance company files with a state that proves a car owner has the state’s minimum car liability insurance requirements.

Collision repair (10% of score): We incorporated insurance company grades from collision repair professionals. We used data provided by CRASH Network, a weekly newsletter covering the collision repair and auto insurance market segments. CRASH Network’s Insurer Report Card used grades from more than 1,100 collision repair professionals to gauge auto insurers on the quality of their collision claims service.

Read more: How Forbes Advisor rates car insurance companies

Compare Car Insurance Quotes

Via Forbes Advisor's Partner

Other Car Insurance Companies We Rated

Here are other car insurance companies we analyzed as part of our best liability-only car insurance companies research.

| Company | Forbes Advisor rating |

|---|---|

3.7 stars

3.7 stars | |

3.0 stars

3.0 stars | |

|

2.8 stars | |

2.3 stars

2.3 stars | |

1.4 stars

1.4 stars | |

|

1.4 stars | |

1.2 stars

1.2 stars | |

|

0.8 stars |

Best Car Insurance Companies 2025

With so many choices for car insurance companies, it can be hard to know where to start to find the right car insurance. We've evaluated insurers to find the best car insurance companies, so you don't have to.

Cheapest Liability-Only Insurance Frequently Asked Questions (FAQs)

What is liability car insurance?

Liability car insurance is the part of a policy that pays others when you’re at fault for a car accident that results in their injury or property damage. Liability insurance also covers your own legal-related costs, including your legal defense, if you’re sued because of a car accident.

Nearly all states require that drivers have at least a minimum level of liability insurance, which is often not enough coverage to properly protect you and your assets.

Should I get liability-only car insurance?

Liability-only car insurance may work for you if you drive an inexpensive car, wouldn’t get it repaired if it was damaged and you’re looking for the cheapest car insurance.

This type of coverage won’t pay to repair or replace your vehicle if it’s damaged, stolen or totaled. If your car gets damaged, you’ll be on the hook to pay for repairs or buy another vehicle if the damage is not worth the repairs.

What is supplemental liability insurance for car rentals?

Rental car companies offer supplemental liability protection (SLP), which covers injuries to others and property damage for accidents that you cause. It’s usually primary to your own car insurance if your personal policy extends to rental cars. Whether your car insurance covers rental cars depends on your policy.

Car insurance typically covers rental cars for personal use at the same coverage limits as your car but may not cover other charges, like a “loss of use” fee. A credit card used for the rental may also offer similar liability coverage. If you have coverage through another source like your car insurance or credit card, you could decline the rental car company’s supplemental liability insurance coverage.

What if my car is totaled and I only have liability insurance?

If you only have liability car insurance and your car is totaled in an accident you cause, your insurance company won’t provide any payout. Instead, you’d have to buy a new vehicle without help from your insurer.

If your car is totaled because you hit another car or object, like a pole, or because of problems such as flooding, hail or fire, you need collision and comprehensive car insurance to cover it. If you’re hit by another driver determined to be at fault, the other driver’s liability insurance should pay to fix or replace your totaled car.