Summary: Best Health Insurance In New Hampshire

Best Health Insurance Companies In New Hampshire

Cheapest Health Insurance by Plan Type in New Hampshire

Health insurance companies that offer health insurance policies on the Affordable Care Act (ACA) marketplace may have four types of health plans. New Hampshire insurers offer two types: health maintenance organization (HMO) and exclusive provider organization (EPO) plans.

- Cheapest HMO in New Hampshire: Anthem Blue Cross and Blue Shield

- Cheapest EPO in New Hampshire: Ambetter from NH Healthy Families

How Much Does Health Insurance Cost in New Hampshire?

Health insurance costs in New Hampshire can vary by age, location, metal tier chosen, whether you smoke and the plan type you choose. Your health and gender aren’t factors in premiums when you get health insurance from the Affordable Care Act marketplace.

Cost of an HMO Plan in New Hampshire

Our evaluation found that HMOs average $411/month in New Hampshire. Here is the average premium for the best health insurance company in New Hampshire.

| Company | HMO cost per month | Learn More |

|---|---|---|

| Harvard Pilgrim Health Care | $455 | On Healthcare.com's Website |

Cost of Health Plans by Metal Tier in New Hampshire

Silver health plans cost an average of $436/month in New Hampshire. Here’s a look at prices among the top-scoring New Hampshire health plans in our analysis.

| Company | Bronze or Expanded bronze plan cost per month | Silver plan cost per month | Gold plan cost per month | Learn More |

|---|---|---|---|---|

| Harvard Pilgrim Health Care | $383 | $479 | $537 | On Healthcare.com's Website |

How to Find the Best Health Insurance Coverage in New Hampshire

Platinum Plans: Good for People Who Expect to Need Frequent Healthcare

Platinum plans are the priciest ACA marketplace plans and they’re also the hardest to find. Less than 10% of ACA plans are platinum plans, so there’s a good chance you might not even see them offered.

If a health insurance company in your region offers platinum plans, these types of plans may work for you if you need frequent healthcare and several expensive prescriptions. These plans have low health insurance deductibles and coinsurance, so you pay less when you receive healthcare. But they also have the highest premiums, so you pay the most for your coverage each month.

Gold Plans: Good for People Who Need Lower Out-of-Pocket Expenses

Gold plans have lower out-of-pocket costs than silver or bronze plans, but they come with higher health insurance premiums. If you expect to get regular healthcare, a gold plan could be a good option since you will pay less when you need care compared to a silver or bronze plan.

You’ll want to balance the monthly premiums with the out-of-pocket costs like coinsurance and deductibles when you’re choosing an ACA plan.

Silver Plans: Good for People Who Are Looking to Balance Premiums and Out-of-Pocket Costs

If you want to avoid very high deductibles but also don’t want to spend a fortune on premiums, a silver plan might be a smart option. Silver plans have lower out-of-pocket costs than bronze plans and lower premiums than platinum and gold plans, which make them a good middle ground.

Silver and bronze plans are the most common ACA plans offered, so you shouldn’t have a problem finding a silver plan in your region.

Bronze Plans: Good for People Who Want the Lowest Premiums

Bronze plans are an excellent option if you don’t use healthcare often and want the cheapest coverage. The trade-off is that bronze plans have higher out-of-pocket costs when you get healthcare.

If you’re looking for the cheapest health plans that still offer comprehensive coverage, a bronze plan could be the best choice.

Some health insurance companies also sell “expanded bronze” plans. These plans come with higher coinsurance levels for in-network care (up to 65%) than standard bronze plans (average of 60%).

More: Bronze, Silver, Gold or Platinum Health Insurance

Catastrophic Plans: Good for Young People Who Don’t Plan to Need Healthcare

The ACA marketplace offers catastrophic health insurance to people under age 30 and those who have severe economic issues like homelessness. If you’re eligible for a catastrophic plan, you may like its low costs but watch out for the high out-of-pocket costs.

One thing that makes catastrophic plans different from other options is that they don’t have coinsurance. Instead, you’ll have to deal with an extremely high deductible when you get medical care. Once you’ve spent that deductible amount on healthcare, a catastrophic plan pays the rest of your in-network healthcare costs for the year.

Methodology

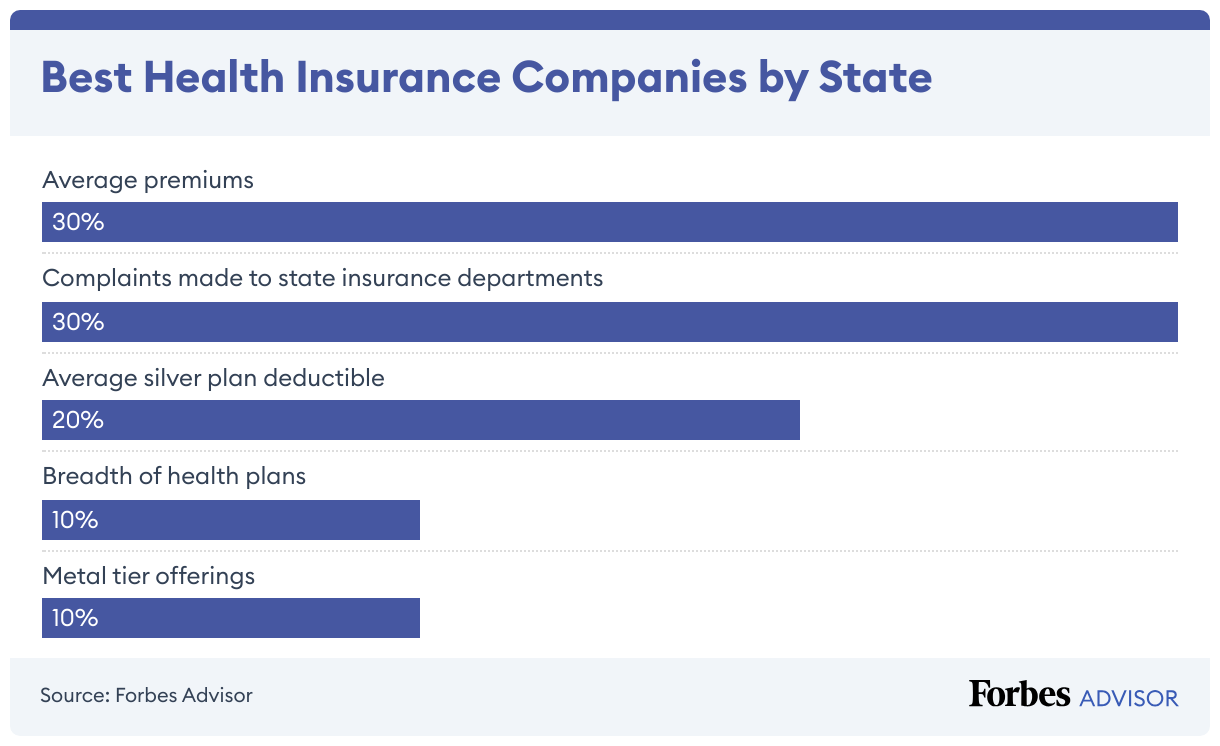

We analyzed Affordable Care Act marketplace health insurance companies in New Hampshire to determine the best options. Our ratings are based on:

- Average premiums (30% of score): We calculated average premiums for health insurance companies that offer ACA plans in New Hampshire. Averages were based on premiums for buyers ages 21, 27, 30, 40, 50 and 60. Source: HealthCare.gov.

- Complaints made to state insurance departments (30% of score): We used complaint data from the National Association of Insurance Commissioners.

- Average silver plan deductible (20% of score): The deductible is how much you have to pay for healthcare in a year before the health plan begins picking up a portion of the costs. Companies with health plans that had low deductibles got more points. Source: HealthCare.gov.

- Breadth of health plans (10% of score): Health insurance companies may offer up to four types of plan benefit designs (PPO, HMO, EPO and POS). We gave points to companies that offer more types of plans. Source: HealthCare.gov.

- Metal tier offerings (10% of score): The ACA marketplace has four metal tier levels. We gave points to companies that offered more tier options. Source: HealthCare.gov.

Read more: How Forbes Advisor Rates Health Insurance Companies

Find The Best Health Insurance In New Hampshire

On Healthcare.com’s Website