About Westfield Homeowners Insurance

Westfield Insurance was founded in 1848 by a group of farmers. The company ultimately expanded beyond insurance for farmers and eventually changed its name to Westfield—named after its headquarters location in Westfield, Ohio.

What Is the Financial Strength Rating of Westfield Home Insurance?

Westfield has an A (Excellent) rating from AM Best.

An AM Best financial strength rating of an insurance company indicates whether the insurer has the ability to pay claims in the years ahead. An A rating from AM Best means the company has an excellent ability to meet its ongoing obligations.

How Much Does Westfield Home Insurance Cost?

The average annual cost for Westfield home insurance is $1,344 for $350,000 coverage. That’s about $330 lower than the national average ($1,678). It’s one reason why Westfield garnered the top spot in our ratings of the best home insurance companies.

Cost by Dwelling Coverage

| Dwelling Coverage Limit | Annual average cost |

|---|---|

| $200,000 | $1,062 |

| $350,000 | $1,344 |

| $500,000 | $1,513 |

| $750,000 | $1,754 |

Cost by Deductible

| Deductible Amount | Annual average cost |

|---|---|

| $250 | $1,289 |

| $500 | $1,289 |

| $1,000 | $1,289 |

| $1,500 | $1,263 |

| $2,000 | $1,236 |

What Types of Coverage Does Westfield Home Insurance Offer?

Westfield home insurance policies provide the standard types of coverage you’d expect.

- Dwelling coverage: Dwelling coverage pays for damage to your house and attached structures (like a deck) due to problems covered by your policy.

- Other structures coverage: Pays to repair or replace other structures on your property, like a shed or detached garage.

- Personal property coverage: Personal property coverage pays to repair or replace your personal belongings, like clothes, toys, rugs and curtains, electronics and furniture, if they’re damaged or stolen.

- Liability insurance: Personal liability insurance pays for property damage and injuries you and your household members accidentally cause to others, such as hitting a ball that breaks a neighbor’s window or a visitor falling due to a loose step. Liability insurance also pays for your legal defense if you’re sued due to an accident covered by your policy.

- Additional living expenses coverage: The additional living expenses coverage within a home insurance policy pays for your extra costs if you can’t live in your home due to a problem covered by the policy, such as fire. It can compensate you for hotel bills, restaurant meals and services like pet boarding or laundry. This is also called loss of use coverage.

- Medical payments: Medical payments coverage pays for smaller medical bills, typically up to $5,000, of people accidentally hurt on or off your property, not including household members. Medical payments coverage doesn’t consider who was at fault.

Options for Westfield home insurance add-ons include:

- Equipment breakdown coverage: Pays to repair or replace certain equipment if it’s damaged by electrical failures, a pressure loss or mechanical breakdowns. These items can include computer monitors and printers, dishwashers, home security systems, refrigerators, sump pumps and washers and dryers. Equipment breakdown coverage is included with the Wespak Estate package or you can add it to a standard or Wespak home insurance policy package.

- Extended replacement cost coverage: Extended replacement cost coverage gives you additional dwelling coverage of up to 25% over the insured value of your house. You get this coverage as part of a Westpak home policy or it can be added to a standard home insurance policy.

- Guaranteed replacement cost coverage: This automatically increases your dwelling coverage to provide any necessary amount for house rebuilding costs, even if it exceeds your coverage limits. Wespak Estate, a package of home insurance coverage for a high-value home, comes with guaranteed replacement cost coverage.

- Identity theft protection: Gives you up to $20,000 for expenses related to fixing identity theft, plus provides resolution services.

- Service line coverage: Pays for the cost to repair or replace damaged exterior underground wiring and piping like electrical, sewer or water lines. It also covers the cost of repairing damaged outdoor property after repairs, including landscaping, driveway and walkways. Service line coverage can pay for a generator if needed for you to remain at home during repairs or the additional living expenses if you must temporarily go to a hotel.

Westfield Home Insurance Packages

Wespak

Westfield’s Wespak package bundles your auto insurance and home insurance coverage into one policy with one bill and one shared deductible. This helps if a single incident—such as a fire—damages your vehicles and house.

Wespak includes additional coverage options, such as:

- Extended replacement cost for dwelling coverage: Provides up to 25% over the insured value of your house.

Freezer content damage: Pays up to $750 for refrigerated or frozen items that spoiled due to a power outage. - Replacement cost for personal property: Pays to replace damaged or stolen items with new, similar items instead of paying only depreciated actual cash value.

- Extra perks: Other perks with Wespak include higher limits on certain personal items—such as firearms, jewelry and silverware if stolen—and additional coverage perks, like debris removal.

Wespak Estate

The Wespak Estate package is for owners of high-value homes and combines home and auto coverages with higher limits than a standard homeowners insurance policy. Benefits of the Wespak Estates include:

- Boat and trailer coverage: Includes up to $5,000 for damage to boats or the trailer used to tow them.

- Come up to code: Pays to bridge the cost difference to bring an older home up to code after repairs or rebuilding that are covered by the policy.

- Cyber insurance: Up to $100,000 of coverage if someone is a victim of cyberbullying or phishing incidents. Includes compensation for money you lost as well as counseling services if needed.

- Disappearing deductible:If you have a deductible of at least $2,500, it goes away if your total claim amount exceeds 10 times your deductible amount. Deductibles less than $2,500 may “disappear” for total losses exceeding $25,000.

- Equipment breakdown coverage

- Freezer content damage: Pays up to $10,000 for refrigerated or freezer contents that spoiled due to a power outage.

- Golf cart coverage: Extends coverage to a golf cart you own.

- Guaranteed replacement cost coverage

- Identity theft and resolution coverage: Pays up to $20,000 for identity theft costs.

- Mold coverage: Pays for damage from mold up to $15,000 with ability to buy up to $50,000.

- Pet damage and injury: Pays up to $5,000 for injuries to or damage done by your domestic pets to your home or vehicle, such as your dog chewing up an antique rug or your pooch being hurt in an auto accident.

- Replacement cash out option: Allows you to cash out and rebuild somewhere else after the total loss of your house, if you so choose. You can also cash out your claim for your home’s contents (personal belongings).

- Sewer or water backup coverage: Pays for damage to your home from a sewer backup, up to $100,000 with an option to buy up to $250,000 of coverage. Also, it will cover up to $5,000 for the cost of labor to install devices that will mitigate future water damage, such as water-leak sensors or automatic shut-off switches.

- Theft special limits: Westfield Estate raises the limits for theft of fur or watches to $25,000, firearms or silverware to $10,000, and cash up to $2,500. Most home insurance theft claims only cover up to $1,500 or $2,500 for such items and only up to $200 for cash.

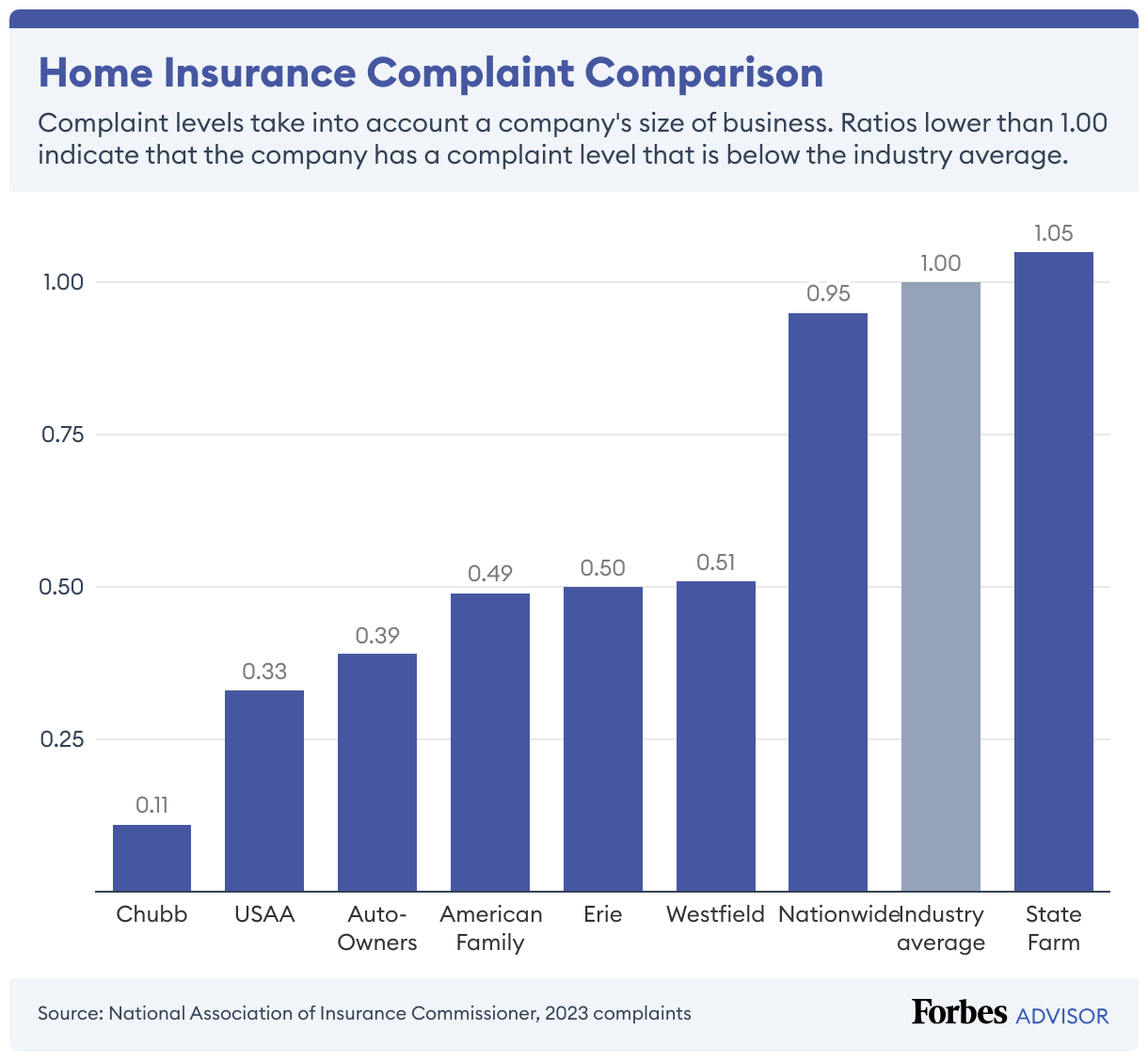

Home Insurance Complaints Against Westfield

Westfield has a very low level of home insurance complaints compared to other insurers, based on complaints made to state departments. Complaints about Westfield home insurance are considerably below the industry average. Westfield’s home insurance complaints relate to policy cancellations and adjusters’ handling of claims.

Westfield Home Insurance Discounts

Westfield offers a variety of home insurance discounts, which can vary by state, such as:

- Account relationship discount: For having both a commercial policy and homeowners insurance with Westfield.

- Alarm and protective devices discount: For having an automatic sprinkler system, a burglar alarm or a fire alarm. You can also get a discount for having both deadbolt locks and a fire extinguisher at your house.

- Loss mitigation devices discount: If you have properly installed and maintained devices that will help mitigate future problems, you can be eligible for a discount if you have the Westfield Estate package policy. You may earn a discount for having a lightning protection system, a surveillance system, a gas leak detector device, a seismic shut-off gas line valve, a low-temperature monitoring device or a water leak detection and shut-off device.

- Multi-policy discount: For customers who bundle home and car insurance with Westfield.

- New home discount: For customers with newly built homes. Homes five years or newer get the best discounts.

- Loyalty discount: For customers who have been insured by Westfield for a specific amount of time without a coverage lapse. The loyalty discount typically starts at three years and may increase the longer you stay with Westfield.

- Prior carrier discount: A discount for being with your previous home insurer for at least three years and with no home insurance claims during that time.

- Senior citizen discount: For those age 55 or older.

- Transfer discount: For Westfield customers who were with their previous home insurer for at least three years.

Comparing Westfield Home Insurance

Price

Westfield has one of the best average prices among the top-scoring home insurance companies in our evaluation. Other insurers, such as Progressive, have lower rates. But Westfield stood out in our evaluation because it has robust coverage offerings and a very low level of complaints.

Home insurance costs vary significantly from one insurer to the next. That means it’s prudent to compare home insurance quotes from multiple companies to ensure you get the best deal for the coverage you want.

| Home insurance company | Average cost per year |

|---|---|

| $729 | |

| $1,157 | |

| $1,256 | |

| USAA* | $1,270 |

| $1,298 | |

| Westfield | $1,344 |

| $1,395 | |

| $1,525 | |

| $1,810 | |

| $2,020 | |

| $2,035 | |

| $2,065 | |

| Shelter | $2,363 |

| $3,220 |

Military and Veterans

Westfield doesn’t perform as well as USAA when it comes to military members and veterans.

USAA, which is only available to veterans, military members and their families, offers perks not found with other insurance companies. For example, USAA covers uniform and military equipment replacement with no deductible for active-duty members. Under certain conditions, USAA also pays up to $10,000 for lost or damaged personal property due to war.

Still, you may find the USAA military-related perks don’t offset another company’s quote or coverage options. For example, Westfield offers guaranteed replacement cost coverage, but USAA does not.

High-Value Homes

Westfield offers the lowest cost home insurance for high-value homes of the companies we analyzed. Westfield’s average rate for $1 million homes is $2,362 annually—nearly half of the national average.

The company also packages together valuable benefits for high-value homes in its Wespak Estate package.

| Company | Annual average home insurance cost for $1 million in coverage |

|---|---|

| Westfield | $2,362 |

| $2,695 | |

| $3,253 | |

| National average | $4,636 |

High-Liability Limits

Westfield can’t compare with Chubb when it comes to high liability limits for home insurance. Chubb, which specializes in high-value properties, has liability insurance limits of up to $100 million. Westfield provides separate umbrella insurance coverage up to $10 million, which might be sufficient for your needs.

On the other hand, Westfield is typically cheaper than Chubb. For instance, our research found that Westfield’s average $1 million dwelling coverage ($2,362) is nearly $3,000 cheaper than Chubb’s average ($5,211). But if your main goal is to find coverage with high liability limits, you should consider contacting Chubb to get quotes for coverage.

Coverage Perks

We gave Erie home insurance high marks for its coverage perks, which are tough to beat. That includes Erie’s Extended Water, which covers natural disaster floods. Home insurance doesn’t usually cover floods. Erie’s SecureHome policies also include add-on options like coverage for misplacing and lost jewelry, watches, silverware and guns.

Westfield also offers many extra benefits, including a home and auto package (Wespak) with a single, shared deductible for claims if one incident damages both your auto and home. The Wespak Estate package, for owners of high-value homes, includes a disappearing deductible.

Extended Coverage for Dwelling

Westfield offers both extended and guaranteed replacement cost coverage. Extended replacement cost coverage allows you to exceed dwelling coverage limits by a specified percentage or amount if building costs exceed your dwelling coverage limit.

Westfield’s extended replacement cost coverage lets you exceed the dwelling limit by 25%. You may get more extended coverage with Nationwide and USAA.

| Company | Offers extended replacement cost coverage? |

|---|---|

| From American Family Connect, starting at $5,000 | |

| Up to 25% more | |

| Up to 25% more | |

| Up to 25% more | |

| Up to 50% more | |

| Up to 20% more | |

| USAA* | Up to 25% or 50% more |

| Westfield | Up to 25% more |

Guaranteed replacement cost coverage goes beyond extended replacement cost. It guarantees that the insurer will pay any amount to rebuild your house after a disaster. Though harder to find than extended replacement coverage, we found that guaranteed replacement coverage is offered by some of the best home insurance companies.

| Company | Offers guaranteed replacement cost coverage? |

|---|---|

| Yes, with American Family Connect | |

| Yes | |

| No | |

| Yes | |

| Yes | |

| No | |

| USAA* | No |

| Westfield | Yes |

Other Types of Insurance Offered by Westfield

Westfield also sells:

- Auto insurance

- Boat insurance

- Business insurance

- Condo insurance

- Motorcycle insurance

- Renters insurance

- RV insurance

Westfield also offers auto insurance, and farm and agribusiness policies.

Methodology

To find the best home insurance, we scored companies based on these factors:

- Home insurance rates (50% of score): Based on average rates for each insurance company for homes with dwelling coverage of $200,000, $350,000, $500,000 and $750,000. Source: Quadrant Information Services.

- Complaints (20% weight): Based on complaints about home insurance that were upheld by state insurance departments. Source: National Association of Insurance Commissioners.

- Availability of extended and/or guaranteed replacement cost coverage (20% of score): Extra dwelling coverage is valuable in the event of large disasters, when construction materials and labor costs tend to spike. We gave points to companies that offer either extended or guaranteed replacement cost coverage. Source: Forbes Advisor research.

- Banned dog lists (10% of score): Banned dog breed lists can make homeowners ineligible for coverage. (A company’s banned dog list might not be applicable in all states.) While any homeowners insurance company could potentially ban any dog with a biting history, not all put a ban on specific breeds. Source: Forbes Advisor research.

Find the Best Home Insurance Companies Of 2025