Types of Nationwide Life Insurance Policies

- Term life

- Whole life

- Indexed universal life

- Guaranteed universal life

- Variable universal life

Nationwide’s Term Life Insurance

Term life insurance has steady rates for a level term period. For example, if you want life insurance to cover income replacement if you die and you have 20 years left before retirement, a 20-year term policy would be an option. After the level term expires, you can renew or buy a new policy, but you should prepare for a significant increase in premiums.

Term life insurance does not build cash value and, as a result, it is often the cheapest life insurance policy type to purchase.

Nationwide YourLife Guaranteed Level Term is Nationwide’s term product offered in level terms of 10, 15, 20 or 30 years for buyers ages 18 to 70 (age limits depend on term length). After the level term period, renewing annually at a higher premium, up to age 95, is an option. The minimum coverage amount is $100,000.

If you decide to convert the term policy into a permanent policy, Nationwide allows you to do that up to age 65. If the coverage is of equal or lesser value, no additional medical exams or underwriting will be required for the term life conversion.

Nationwide’s Guaranteed Universal Life

Guaranteed universal life insurance offers the potential for flexible premiums and death benefit amounts, up to specified limits, but the ability to accumulate cash value could be minimal. Since policyholders can expect minimal gains from this type of life insurance, it is usually cheaper than other universal life products.

Nationwide No-Lapse Guarantee UL II is Nationwide’s universal life insurance option targeted for affluent clients with low risk tolerance. It is available to people up to age 85 and with a minimum face amount of $100,000. This low-risk product comes with two no-lapse guarantees, one for the initial period and one for an extended period that can be customized to up to age 120.

Nationwide’s Whole Life Insurance

Whole life insurance works as an option for people looking for a low-risk life insurance policy with fixed premiums and guaranteed cash value accumulation.

Nationwide Whole Life 100 is one of three whole life products sold by Nationwide and is available to people ages 0 to 80. Minimum face amounts range from $10,000 to $250,000 depending on your health classification, which the insurance company determines. You can continue paying fixed premiums on Whole Life 100 until you reach age 100. You are guaranteed the full death benefit if you die unless you have borrowed or withdrawn against the cash value. In that case, the death benefit is reduced by whatever you owe. If you make it to age 121, Nationwide will pay out the death benefit and cease coverage.

Instead of fixed premiums until age 100, Nationwide 20-pay Whole Life offers a guaranteed death benefit if you pay the fixed premium for the first 20 years and take no withdrawals or loans against the cash value.

Nationwide Simplified Whole Life is an option for people who have purchased an eligible Nationwide auto and/or homeowners insurance policy. It offers basic protection between $10,000 and $50,000, a simplified application and no medical exam requirements.

| Nationwide Whole Life 100 | Nationwide 20-pay Whole Life | Nationwide Simplified Whole Life | |

|---|---|---|---|

| Best for | Those seeking traditional whole life insurance with all the guarantees | Those seeking traditional whole life insurance with an easier application process | Existing Nationwide clients seeking low coverage life insurance without a medical exam |

| Death benefit | $10,000 to $250,000 minimum | $10,000 to $250,000 minimum | $10,000 minimum to $50,000 maximum |

| How to apply | Through a broker | Through a broker | Through a broker |

| Available for applicants | 0 to 80 years old | 0 to 80 years old | 0 to 80 years old |

Nationwide’s Indexed Universal Life Insurance

If you’re looking for a death benefit that will grow with an index, like the S&P 500, indexed universal life insurance (IUL) is an option. This type of life insurance links your cash value to an index. It includes participation rates, caps and floors that may keep the policy from the biggest gains and losses.

IULs also offer the flexibility to vary premiums and death benefits and take withdrawals or tax-free loans against the cash value. However, keep in mind that if your cash value gets too low to cover policy expenses and fees, the IUL policy could lapse.

Nationwide Indexed Universal Life Accumulator II is a life insurance product focused on cash value accumulation and available to buyers ages 18 to 85. It is offered with a minimum $100,000 face amount and two cash accumulation investment strategies. You’ll have the option of a fixed interest strategy with a guaranteed minimum interest rate of 1%. Or, for a higher risk option, you can choose an indexed strategy tied either to the performance of the S&P 500 or a combination called the Multi-Index Monthly Average, including S&P 500, Nasdaq-100 and the Dow Jones Industrial Average.

The IUL Accumulator II includes a participation rate of 100%, a floor rate of 0% and a cap between 9% and 13%, depending on the investment strategy you choose.

A participation rate is the percentage of the index performance used to calculate your interest crediting rate. For example, if the participation rate is 100%, then 100% of the index gain will be credited to your cash value, up to your cap rate.

A floor rate is the guaranteed minimum rate that protects your cash value from loss, no matter how the market performs. Your loss can’t dip below this amount, so it is called a “floor rate.”

Nationwide also offers an IUL focused more on protection than accumulation called the Nationwide Indexed Universal Life Protector II.

Nationwide’s Variable Universal Life Insurance

Variable universal life (VUL) insurance comes with various features, including cash value investments with sub-account choices, the flexibility to vary premium amounts and frequency of payment and death benefit options.

This permanent life insurance is intended to stay in place throughout your lifetime. VUL insurance includes the ability to borrow tax-free or withdraw from your cash value but can lapse if your cash value gets too low to cover policy expenses and fees. VUL insurance policies typically include significant fees and are best suited for people comfortable with higher risk because of the investment component.

Nationwide Variable Universal Life Accumulator is available to buyers up to age 85 with a minimum face amount of $100,000. Its main purpose is cash value accumulation. Policyholders can choose from three investment strategies: the S&P 500 Annual Point-to-Point, One-Year Uncapped S&P 500 Point-to-Point, and a Multi-Index Monthly Average that combines the S&P 500, Nasdaq-100 and Dow Jones Industrial Average. The cap rate, participation rate and floor depend on which investment strategy you choose. For example, if you go with the S&P 500 Annual Point-to-Point, the participation rate is 100%, the cap rate is 8.5% and the floor is 1%.

Nationwide’s protection-based version of the VUL Accumulator is the Nationwide Variable Universal Life Protector.

How Much Does Nationwide’s Insurance Cost?

Nationwide’s Guaranteed Level Term costs an average of $173 a year for a 20-year, $250,000 policy for a healthy 30-year-old female buyer, based on our analysis. That’s higher than some other top companies but still competitve.

Nationwide’s Term Life Insurance Rates vs. Top Competitors

Nationwide’s YourLifeGLT costs an average of $225 a year for a 20-year, $500,000 policy for a healthy 30-year-old female, based on Forbes Advisor’s analysis. That’s higher than most other top companies.

Here’s a comparison of Nationwide’s term life insurance rates to top competitors.

| Company | Term life insurance policy name | Cost per year: Female buyer age 30, $250,000 for 20 years | Cost per year: Male buyer at 30, $250,000, 20 years |

|---|---|---|---|

| Guaranteed Level Term | $173 | $180 | |

| PL Promise Term | $128 | $145 | |

| Classic Choice Term | $127 | $144 | |

| Term Essential | $168 | $185 | |

| TermAccel | $134 | $152 | |

| Term Life Answers | $155 | $170 | |

| Non-Convertible Term | $127 | $145 |

Nationwide’s Term Life Insurance Rates by Age and Amount

| Coverage | Buyer age 30, cost per year | Buyer age 40, cost per year | Buyer age 50, cost per year |

|---|---|---|---|

| $500,000, 20-year term life insurance | Female: $225

Male: $260 | Female: $310

Male: $365 | Female: $660

Male: $885 |

| $1 million, 20-year term life insurance | Female: $375

Male: $445 | Female: $535

Male: $635 | Female: $1,215

Male: $1,665 |

Nationwide's Life Insurance Riders

Life insurance riders are options for buyers who want to customize a life insurance policy with extra coverage or features. Rider availability may vary by policy type. Here are the riders offered by Nationwide.

- Accidental death benefit rider. Nationwide’s Accidental Death Benefit rider gives beneficiaries an additional death benefit, on top of the base policy death benefit, if the insured’s death is caused by an accident.

- Children’s term insurance rider. Nationwide offers a child life insurance rider for term policies that include a death benefit for your minor children ages 15 days to 22.

- Chronic illness rider. This rider allows you to receive a portion of your death benefit early if you are diagnosed with a permanent chronic illness that results in an inability to perform at least two of six activities of daily living (ADLs).

- Critical illness rider. If you are diagnosed with a critical illness, like cancer or a heart attack, this rider allows you to receive a portion of your own death benefit.

- Early/enhanced cash value rider. This rider can adjust surrender chargers to offer higher surrender values if you need to surrender your policy within the first few years.

- Estate protection rider. This rider helps offset estate taxes that may be due if the life insurance payout goes into the insured person’s estate.

- Guaranteed insurability rider. This benefit ensures the policyholder can purchase an additional life insurance policy after proving insurability on each option date (specified in the policy).

- Lapse protection rider. Nationwide’s No Lapse Guarantee Rider ensures that the policy will not lapse or terminate during the rider period as long as certain premium requirements are met. This rider is issued at no extra charge with all permanent policies.

- Long term care rider. This rider accelerates part of the death benefit if long-term care is needed.

- Overloan protection rider. This rider helps prevent lapses if you borrow money from your cash value and there isn’t enough left to cover policy fees.

- Return of premium rider. If you outlive your term life insurance policy, Nationwide’s Return of Premium Death Benefit rider will refund a specified percentage of the premiums you’ve paid after the initial term length.

- Terminal illness accelerated death benefit rider. Nationwide’s Accelerated Death Benefit rider makes your death benefit available early if you become terminally ill and have 12 months or fewer to live.

- Waiver of monthly deduction rider. Nationwide’s Disability Waiver helps by waiving monthly deductions when you can prove disability for at least six continuous months.

- Premium waiver rider. This disability rider credits a monthly premium to your policy if you cannot work as a result of a disability lasting at least six months.

How Do I Buy Life Insurance From Nationwide?

How to File a Claim with Nationwide

You can start the claims process with Nationwide by filling out the form on the company’s website. You can also call customer service at (800)-848-6331.

Get A Quote From Nationwide

Via Policy Genius' Secure Site

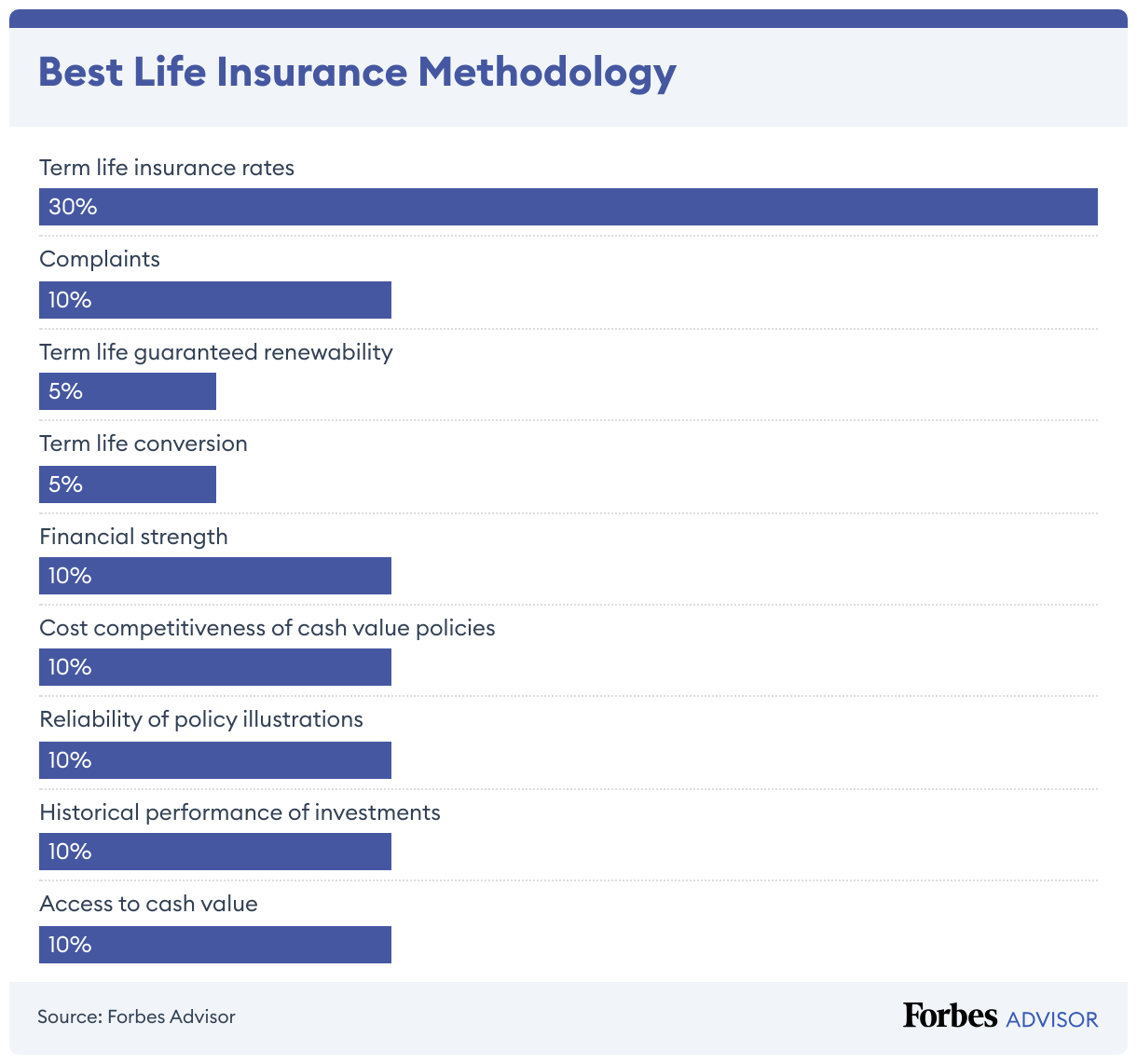

Methodology

To find the best life insurance companies, we evaluated term life and permanent life insurance for each company. We used our own research and data courtesy of Veralytic, a life insurance analytics provider that rates cash value policies based on their overall competitiveness. Veralytic’s data provides a unique depth to Forbes Advisor’s analysis of whole, universal, indexed universal and variable universal life insurance policies from each insurer. Veralytic reports are available through financial advisors.

Our analysis was based on the following.

Nationwide Life Insurance Frequently Asked Questions (FAQs)

Can I cash out my Nationwide life insurance policy?

If you have a Nationwide cash value life insurance policy with sufficient cash value, you can surrender the policy and receive your cash value minus any surrender charge.

You cannot cash out a term life insurance policy as there is no cash value.

Do Nationwide whole life policies pay dividends?

Nationwide is a stock company and does not pay dividends on its whole life policies.