Navigating credit and debt with poor credit can be challenging. Although it’s important to avoid predatory options like payday loans and high-interest installment loans, there are steps you can take to get a loan with bad credit.

As you look for options to get a loan, compare different lenders and be sure to understand the terms and conditions of any loan before accepting it. Some lenders try to take advantage of borrowers in desperate financial situations, but these loans can land you in a cycle of debt.

What To Know Before Getting a Loan With Bad Credit

Getting a loan with bad credit can be challenging, as lenders typically view individuals with bad credit as high-risk borrowers. If your credit score is poor—your FICO score is below 580—lenders may be less willing to approve your loan application, or they may charge you higher interest rates or require collateral to back your loan.

Although it can be tempting to turn to just any loan that doesn’t require a credit check, these loans can also come with many risks. These loans, often marketed to those with poor credit histories, typically come with extraordinarily high interest rates and fees.

If you fail to repay one of these loans on time or start missing payments, the debt can grow due to the interest and fees. Eventually, that can lead to taking out other loans to cover previous debt, which can trap you in a cycle of debt.

Before accepting any loan, be sure to understand the interest and fees that come with the loan and the loan terms. Beyond that, a loan calculator can help to estimate what your payments could be so you can be sure those payments fit into your budget.

How To Get a Loan With Bad Credit

Getting a loan with bad credit is often more difficult than qualifying with a credit score of 670 or above. Still, there are steps you can take to simplify the process, improve your approval odds and qualify for the best rates available to you.

1. Understand Your Credit Score

Your credit score reflects your creditworthiness, and it’s the first thing lenders consider when you apply for a loan. If you have bad credit, look to understand why. Obtain a copy of your credit report and scrutinize it for errors or discrepancies that could negatively affect your score. If there are errors, contact the three major credit bureaus to correct them.

Understanding your credit score can also give you insights on how to improve it. There are several factors that make up your credit score, and lowering your credit utilization rate, for example, can help increase your score.

2. Improve Your Credit

Improving your credit score isn’t a quick process, but it can be essential to secure favorable loan terms. You can improve your credit by paying your bills on time, reducing the debt you owe and not opening too many new credit accounts.

3. Research Potential Lenders

Not all lenders look at bad credit in the same way. Some specifically work with borrowers with bad credit and look closer at other aspects of an application, such as income and college education. The lenders that offer the best bad credit loans often look beyond your credit and offer loans with competitive interest rates.

Keep in mind, lenders that work with borrowers with bad credit often offer high interest loans, so be sure you understand the rates and terms of a loan before accepting it.

4. Prequalify for a Loan

Before submitting a loan application, try to prequalify with multiple lenders. This allows you to see the rates and terms you may qualify for without impacting your credit score. Comparing prequalification offers can be an effective way to find the most cost-effective loan option.

| COMPANY | LOAN AMOUNTS | MINIMUM CREDIT SCORE |

|---|---|---|

| Upgrade | $1,000 to $50,000 | 600 |

| LendingClub | $1,000 to $40,000 | 660 |

| Upstart | $1,000 to $50,000 | 620 |

| LendingPoint | $1,000 to $36,500 | 600 |

| Avant | $2,000 to $35,000 | 580 |

| OneMain Financial | $1,500 to $20,000 | OneMain Financial does not disclose this information |

5. Apply for the Loan

Once you’ve done all the preparatory work, it’s time to apply. Be ready to provide all necessary documentation and follow up quickly in case any other information is needed. Remember, a rejection doesn’t mean the end—it just means you need to keep looking for the right lender.

6. Consider Co-Signers or Collateral

If you’re still struggling to secure a loan, consider enlisting the help of someone with a better credit score as a co-signer. A co-signer is responsible for the loan if you cannot make payments. Alternatively, you could offer collateral, such as a car or property, to get a secured personal loan. These options may increase your chances of approval.

Where To Get a Loan With Bad Credit

Securing a loan with a less-than-perfect credit score can take time and effort. However, several avenues are available, each with pros and cons. These are some options for where you can get a loan with bad credit:

Credit Unions

Online Lenders

Traditional Banks

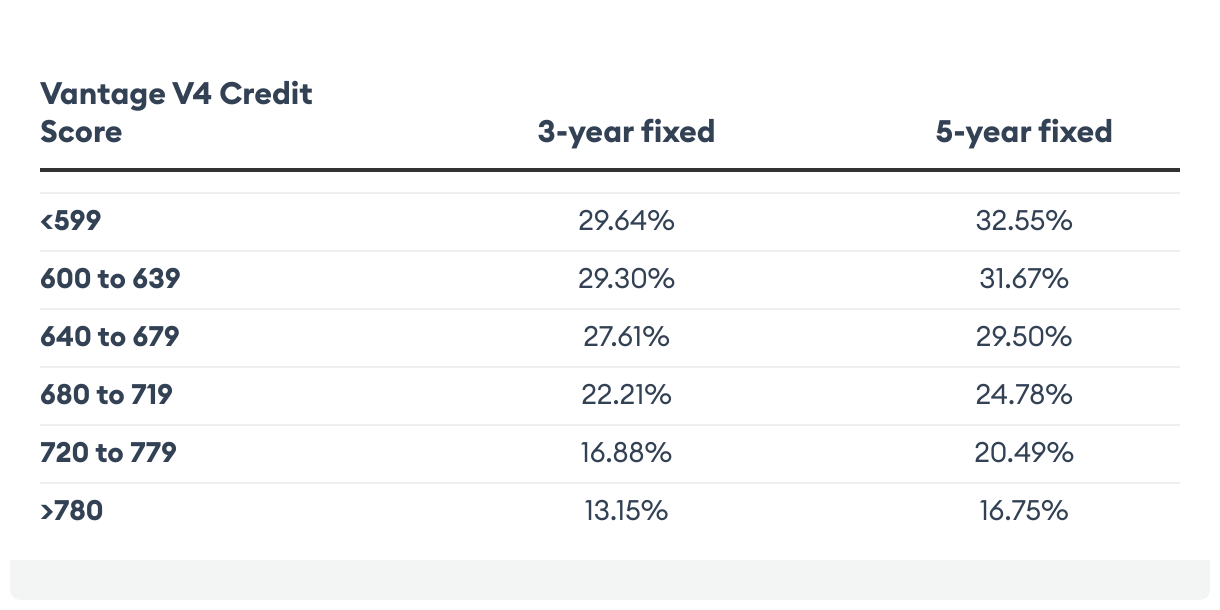

Average Interest Rates for Borrowers With Bad Credit

According to Credible, the average interest rates for Vantage Score ranges are as follows:

Alternatives to a Loan With Bad Credit

Although it may seem like a loan is your only option, there are alternatives to a personal loan that may work better for your financial situation. Some alternatives include:

- Credit card cash advance. Credit card cash advances let you withdraw cash directly from your credit card. It can be a quick and easy way to access funds, especially in emergencies. However, interest rates are typically higher than other financing options and interest starts accruing immediately with no grace period.

- Peer-to-peer (P2P) lending. P2P lending is a form of financing where individuals can borrow and lend funds without needing a traditional financial institution as an intermediary. P2P lending can offer more flexible terms than traditional lenders, and your credit score may not be as significant a factor.

- Friends and family. Borrowing from friends and family can be a viable option if you have bad credit. It provides an opportunity to obtain a loan with more favorable terms, such as flexible repayment plans, lower interest rates or no interest rates at all. If you pursue this option, ensure the terms and conditions are clear.

- Credit counseling and debt management plans. These services, often provided by nonprofit organizations, can help you improve your credit score and manage your debt over time. Credit counselors can assist you in creating a budget, negotiating with creditors and developing a debt management plan.

- Paycheck advance. Some lenders offer paycheck advances or emergency loans. A paycheck advance lets you access your earned wages before your scheduled payday. While it can be convenient to cover unexpected expenses, only use this option sparingly to avoid becoming reliant on future earnings.

Compare Personal Loan Rates From Top Lenders

Compare personal loan rates in 2 minutes with Credible.com

Frequently Asked Questions (FAQs)

What is the easiest loan to get with bad credit?

The easiest loans to get with bad credit are typically secured loans or personal loans from credit unions. Secured loans require collateral, or something of value to back the loan, while credit unions often have more flexible lending criteria.

Does getting a loan with bad credit affect your credit score?

Getting a loan with bad credit can impact your credit score. When you apply for a loan, lenders perform a hard credit check that may temporarily lower your score. How you manage the loan—like making timely payments or defaulting—will significantly influence your credit score over time.

How long does it take to get a loan with bad credit?

The time it takes to get a loan with bad credit varies. Online lenders usually offer initial lending decisions within a few hours to a day, while traditional lenders may take several days to process applications. Factors such as documentation and lender responsiveness can also influence the overall timeline.